and what are we seeing on the dashboard?

by Chisom Uche and Evan Thorpe

Does a pandemic hasten or pause changes already underway in wealth management? Given the foundational basics in which the wealth management sector is grounded, one would think that COVID-19 would not alter the course of that industry’s trajectory in a major way. That grounding: the personal relationship between a client and their advisor still means something and the fact that clients have been willing to pay advisors to partner with them in securing their long-term financial well-being. A global pandemic does not necessarily turn such a model inside-out; or at least, not singlehandedly.

The wealth management industry has already been on a journey of transformation and so at this particular juncture in that evolution, we are interested to know: what impact will COVID-19 have on the character of that transformation in the near-term?

Wheels Already in Motion, Pre-COVID

The digital revolution marched on. Alternative advisors and brokerages (Betterment, Robinhood, Motif, Acorns, etc.) and personal financial management tools (such as Mint, YNAB, Clarity Money / Marcus) are years into their iterations on offering personalized financial services at lower cost and, in doing so, opened up more options for individuals seeking a partner. These new market entrants looked beyond accruing assets towards acquiring more data under management, and prioritized relationships via their client’s information. They have begun to act on this data with increasingly individualized service. This has created additional pressure on incumbent advisors to prove that the value of their service justifies their fees.

For example, one such plot line already in motion: all wealth management players -including those grounded by years of experience and those experiencing recent but viral growth,- will continue to pursue better solutions that aid their adherence to new and evolving regulations and controls aimed at protecting an emerging “asset under management”: clients’ digital identities. But this was already occurring pre-COVID; so, what now?

Beyond identifying these pre-existing sectoral shifts, we ask: what occurs when COVID-driven shifts expose and compound industry challenges?

In addressing this question, our investment team drew up a lens we could use to examine the impact of COVID-19 on each of the categories and industries in which we operate, collaborate, and invest: FinTech, InsurTech, Digital Health, Data Security, and related subcategories, including WealthTech.

We believe that such impact is not driven by one singular force but rather a bundle of multiple forces which are influencing the operational character of these categories, and the prospects for the startups reshaping them. See endnote* and our accompanying Medium article for more on our methodology.

At the end of the day, the purpose in developing this lens is to draw out further observations about our sub-sectors and their value chains so that we may make better decisions as investors and as collaborators working alongside industry incumbents and startups, alike.

Social Distancing Favors the Tech-Enabled & Incumbents Revisit their Differentiators

Where COVID-19 drives dispersal of people and resources, the new reality of social distancing brings a collective rethink of how advice is administered. Digital solutions already have a head start in architecting platforms that deliver value regardless of how dispersed individuals may be. By utilizing tools that acquire, onboard, and service users without the need for human interaction, they are in a position to handle, or even benefit from, a distributed client base. These tools, however, are largely administrative in nature and one asks: what about the advice? Meanwhile, traditional wealth managers now need to adjust how they establish and maintain relationships and deliver advice to their clients without face-to-face interactions.[1]

Self-service capabilities offered by robo-users typically attract the younger, less affluent, and more risk-taking user profiles. While these users tend not to fall within the traditional wealth manager’s target demographic today, they are still prospective clients with potentially enormous value. Users of robo-solutions may graduate to a more traditional advisor as their financial needs and lives become more complex and as their financial and health needs develop. Even if such users do graduate in this manner, the bar for what they deem an acceptable client experience has been set at a height above that which is currently provided by most traditional advisors.

It prompts the question: what technology-enabled groundwork do incumbent wealth advisors need to lay in the current market context in anticipation of emerging customer segments and what can they do today to influence these individuals to sign on as customers, tomorrow?

The Impact of Greater Digital Volume

The more that employees, wealth managers, and their clients are physically dispersed, the greater the chance that their online footprint has increased. The increased digital volume wrought by these now-online interactions presents both a challenge and an opportunity for how institutions think about the impact of COVID-19.

On the table for discussion is their approach to data under management, customer data security, digital throughput, etc. Standing between these questions and a clear solution, however, lie multiple layers of operational and technological barriers. Incumbent wealth managers seeking to realize improved capabilities unlocked by leveraging data insights from client information know this puzzle well.

Solving tactical but sizable problems such as how to shift away from manual and paper-based processes for how data is generated, collated, and parsed is now table stakes for any players trying to assess the even deeper (and more exciting) problems.

A number of forward-thinking wealth managers and brokerage platforms that have adopted data analytics have harnessed the ability to identify clients that are most vulnerable during an economic crisis, thereby significantly reducing the time and cost required to prove their value to those clients. Step one involves prioritizing and resourcing the capabilities that support these insights. If step two will translating these insights into actions; then perhaps a meaningful step one-and-a-half wedged in between is asking the question: which functions should be the first selected to become more insight-driven?

Will players select distribution and service as the most deserving areas for this type of enhancement? Among incumbents and robo-platforms alike, the capacity for wealth managers to proactively engage clients -irrespective of their relative profitability- and help them to solve for their financial future strikes to the core of personalized service generative to customer loyalty. But in a market where all players are moving in the direction of tech-enabled change, how can any given player select an appropriate differentiating strategy? Double-down on brand, service, and relationships? Raise the bar for the state-of-the-art analytic capabilities? If both, how might these firms go about ensuring that the bridge extending from each of these two sides effectively meets in the middle to mutually support each other?

If players prioritize client engagement above all else, there still remains the need to disseminate personalized and timely communications in a mode appropriate to the audience and the current climate. In years previous, it may have not seemed possible for people to spend more time looking at their screens than they already do. But now, with an increase in people staying indoors, COVID-19 has prompted even more client requests, social media marketing, automated marketing, and other digital interactions. Chatbots will be more valuable to both robo and traditional advisors in terms of managing the opportunity for increased quantity of communication, but can AI-driven chatbots and conversational utilities keep up with a need to improve quality where users face device burnout? Could the isolation of shelter-in-place cause people to value a personal touch to a greater degree and cheapen the utility of bots?

Bolstering digital communication capabilities as we have transitioned to remote working also requires increased investment in information security, especially in an industry like wealth management where the mismanagement of client information rightly carries hefty consequences. While manual or paper-based processes kept information offline and safe, the now reluctance to send or handle physical paper will add further pressure to digitize as much of the business as possible.

Though this is not as eye-catching as better customer engagement and product distribution, perhaps the downside risk of under-resourcing data security may yet warrant simultaneous revisiting; an expensive but important exercise. A greater focus on customer data markedly increases the need to further invest in data security and so the total price of capturing customer insights comes into focus.

We believe that incumbent players have not only the more immediate need to invest in robotic process automation (RPA), data ingestion, customer relationship management (CRM), and back-office automation solutions, but an equal if not greater need to invest in the corollary: identity verification, data security, anti-phishing, and information access capabilities.

Fighting Inertia: The Slowed Movement of Capital & Resources[2]

Growth at scale in wealth management is fueled by the influx and movement of capital. As a result, a threatened economic recession could present a severe problem for the industry. Robo players, one could argue, present a lower barrier to entry for new capital, but risk becoming ‘one-trick-ponies’ that cannot offer much investment flexibility. A potential result: their success hinges almost entirely on the AUM of their customer base. Incumbent players need AUM just as intensely (if not more, given their cost base), but since they also generate revenue through the personalized services and flexibility that their clients are willing to pay for, their equation is not so straightforward. For example, when markets stall and clients seek to alter their portfolios, traditional advisors stand to be in a better position to service their current client base. However, with a stalled job market, new prospective clients may not meet the prerequisite asset levels required by a traditional advisor and may end up with a robo-solution by default.

The current environment has broken the previous formulae for an ‘ideal portfolio construction,’ regardless of whether they are fixed and algorithm-based or developed through a series of face-to-face conversations. The new normal is still up-for-grabs.

Segmentation: FinTech Startups are Unbundling, Too

Industry revolutions and the unbundling of business models typically go hand-in-hand. Regulation and legacy incumbency, however, has provided wealth management players protection from externally driven revolutions. As a result, the sector has historically been insulated from drastic reconstruction but is nonetheless prone to unbundling. In the present day, the industry’s value chain is experiencing segmentation of an internally driven nature: reorganization. In a post-COVID-19 context, back and middle office operations within managers will continue to revisit how they share data across disparate locations so that data sharing and collaboration can take place effectively and also compliantly.

The division of labor required to do so, however, need not take place entirely under one roof and third-party players may be able to specialize. In other words, firms, service providers, and advisors can each stick to doing what they do best and focus. These operational shifts are increasingly a tactical necessity to maintain profitability and it is not just incumbents driving these initiatives, but startups as well. One way some emerging tech players may do so is by providing platforms that make the compliant sharing of data among various third parties possible while keeping costs low.

Startups in the wealth management space are unbundling, also. Tech-enabled services such as robo-consultations, conversational customer services, dynamic portfolio rebalancing utilities, and investor onboarding functions have each become sub-categories among wealth management FinTech firms with each sticking to their own focused niche.

Re-positioning and Survival

As the progression from COVID-19 shock shifts to business-as-usual, what changes will endure and persist? For startups and incumbents, certain key questions are already coming to the fore: What will be the impact of COVID-19 on client investment portfolio performance? What customer behaviors could result from that performance, and how can we get out in front of these? Will the robo-client base eventually graduate to a traditional advisor, as expected by many? If so, we may see more acquisitions of robo-solutions from traditional players or may see third parties offer solutions that could supply pieces of these capabilities, a la carte. On the other hand, we may see robo-solutions expand their offerings to broader services in a play to retain the clients they have acquired during the pandemic.

Alternative assets are already seeing a large increase in popularity and uptake and ESG is developing at an impressive rate. Will a COVID-19 setting combined with the accompanying economic conditions that follow inspire deeper interest in emerging asset classes on the rise?

Emerging Opportunities in Wealth Management & WealthTech

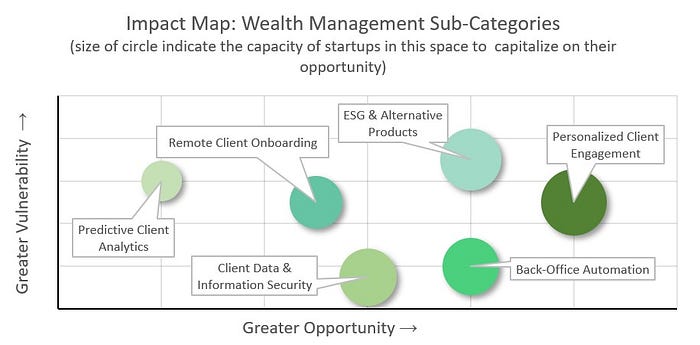

The graph below compares at a high level five emerging sub-categories in wealth management experiencing both opportunity (x-axis) and vulnerability (y-axis) amid the COVID-19 pandemic.

The farther the circle is to the right, the greater near-term opportunity we believe sits ahead of them. The higher the circle is toward the top, the greater vulnerability they may experience amid the current context of the pandemic. The size of each sub-category’s circle indicates the greater or lesser potential for players (including startups) in that sub-category to capitalize on the opportunity. In short: which sub-categories could be primed for big shifts (good or bad) and are the current players (broadly speaking) in that space in a position to do something about it?

We see wealth management incumbents as well as FinTechs doubling down on personalized client engagement services and we may see no better time for those players to offer enhanced customer experience than today in a socially distanced world where face-to-face contact is not the norm. In parallel, emerging startups and wealth management mainstays alike, may be finding that ESG and alternative products present great opportunity but multiple players crowding into these areas simultaneously could bring vulnerability in the form of commoditization risk.

Given the reset of customer habits driven by COVID-19 and the reset of client expectations of markets, it could also be opportune to expand customers’ concept of what wealth management and financial planning can comprise. If it is indeed the case that clients are now quite amenable to new products, new formats, delivered in different ways, we ask: how long will that interest hold if the market regains its composure as people go back to work and assume lifestyles that resemble those of pre-COVID-19 times? How will those factors impact wealth advisors’ ability and motivation to modernize legacy processes and systems? And who will step up to lead that charge?

*Our methodology involved drawing out 5 basic forces impacting FinTech, InsurTech, Digital Health, Data Security, and their various sub-categories. The basic forces that rose to the top: Dispersal, Inertia, Digital Volume, Segmentation, and Survival. We then asked questions about what happens when these forces meet the plot lines already in motion in each of these categories. This is not an exhaustive list of forces impacting these markets and there are also multiple levels of granularity at which we could classify or group these impacts. In keeping the scope manageable, we limited the forces we are using as a lens to 5. These are the 5 that rose to the top as we examined what was on the minds of our founders and our LPs as we looked to align with each on navigating the uncharted waters ahead.

[1] https://www.finextra.com/blogposting/18646/what-are-the-key-strategies-and-tools-to-help-wealth-management-through-the-coronavirus-pandemic

[2] https://www.wealthmanagement.com/advisor-channels/ripple-effects-independent-bds-post-covid-19-world

Photo credit: Benjamin Child on Unsplash