In the Post-COVID Financial Institution, Enterprise Infrastructure takes Center Stage

What Questions Should we Ask about the Breakout Stars and the Reluctant Understudies?

By Joel Brightfield and Evan Thorpe

We all have seen the headline: Software Eats World. Looking back, the path and trajectory of Software-as-a-Service looks obvious. Against a COVID-19 backdrop, the tailwinds behind this trend pick-up and we ask: What specific currents come in to focus here? How are they shaping the nature of the uptick in enterprise software investing?

At SixThirty, we examined our thesis for investing in enterprise financial technology infrastructure, and our investment team pressed the forces that comprise the COVID-19 shifts up against the space. We looked at the forces of: Dispersal, Digital Volume, Inertia, Segmentation, and Survival to see what themes emerged that inform our expectations for the direction of this sub-category.

“Enterprise financial technology infrastructure” are four important words when put together. We are talking about the technological foundation that powers the financial services industry.

We are talking about the technical infrastructure that fuels the movement of money and securities, the settlement and reconciliation of transactions, omni-channel experiences, and so on. We are also talking about physical infrastructure (e.g., on-premises computing, cash, branches, etc.) and cloud infrastructure (e.g., computing power, security, etc.).

Infrastructure is a massive sub-category of financial technology which, by itself, cannot be painted with one brush. And the nuances of COVID-19’s effects at the product and feature level cannot be underestimated. But let’s take a look at it. In order to get our arms around the space, it is essential to breakdown the themes –at least at a high level- in order to chart how the foundation of the industry may shift as a result of the pandemic, and where the opportunities may lie going forward.

Before diving into the impact of COVID-19, let’s get acquainted with the category by looking at some well-known examples of financial technology infrastructure companies. As (overly) simplistic examples, Plaid and Stripe are companies that everyone in FinTech has heard of, but no one else has. Plaid’s infrastructure powers the connections between hundreds of third-party apps and a consumer’s bank account. Visa recently came close to acquiring the company for billions. If you have a Robinhood account, then you’ve used Plaid; if you have purchased a ride on Lyft, then you have paid for it through Stripe.

The most recent private market valuation for Stripe was $95bn, with some arguing that despite the apparency of something exceptional, perhaps it should not be seen as all that remarkable, given the category’s rise, overall.

With not just a couple of companies cropping up but an entire industry on the rise, let’s assess the state of the category against the backdrop of a post-COVID context. Let’s look at what emerges as good and bad; as opportunity and risk.

Dispersal: Sudden Stress on BAU Protocols in a Distributed Environment Pushes Enterprises to (re)Evaluate their Stack Capabilities

The manner in which we interact with financial services was turned upside down overnight as a result of COVID-19. The force here was dispersal as physical transactions and processes moved online and those transacting had to go remote. For example, transactions usually done in-person at a branch of a bank or brokerage, or trading activities typically done on a crowded trading floor had no choice but to move online. Call center employees and the firms they support had to set up makeshift (perhaps now permanent?) in-home call centers. The movement of these functions stressed the system as it existed. The dispersal of financial services stressed the industry’s technology infrastructure in the context of business continuity plans -namely network connectivity- with security of transactions and processes being completed “off premise,” and remote communications becoming the norm, rather than the exception. Mobile/omni-channel capabilities were thrust into the spotlight, and those without such capabilities were exposed and forced to play catch up.

Digital Volume: Where Pipelines Carry Greater Digital Volume, Missed Opportunities Could Come into Greater Focus

Is the shift to capitalize on digital opportunities a matter of winners and losers? Commentary on the spike in digital volume is ubiquitous: mobile banking surges 200%[1], Microsoft Azure beats estimates,[2] AWS lead earnings reports[3], etc.

There certainly appear to be winners. So, are there also losers?

Perhaps the more telling headlines are those placing a spotlight on processes that remain completely offline. The ever-persistent threat of industry insurgents is accentuated in a post-COVID environment.

Take, for instance, the Paycheck Protection Program (PPP). The fact that in 2020, the U.S. Government did not have a way to deposit stimulus funds into the bank accounts of U.S. citizens was striking. Challenger banks, the earliest of which are approaching 10–15 years old, and other venture-backed fintech companies were tapped to help process the PPP volume.

Similarly, in insurance, when incumbents made the admirable decision to refund premiums, by and large, the refunds were processed via paper checks. Will modern-day, full-tech-stack InsurTech companies seize the opportunity to capture the uptick in interest among consumers for a fully digital insurance experience?

At a more basic level, has COVID-19 hastened an intermingled flow of digital volume and financial volume and thereby blurred the lines between digital capabilities and financial capabilities? One thing that is certain is the growing mismatch between offerings and capabilities both of a financial and a digital nature (across the front-end and back-end) has pushed institutional incumbents further in their need to reassess value chains. For those institutions who have explored this already, pre-COVID, a deep dive could be in order: deliberate identification of which strengths and which vulnerabilities derive from their infrastructural capabilities.

Inertia: The Imperative and Consensus for Adaptation Bumps up against Institutional Inertia

As quickly as the industry found itself in unchartered territory, the conversation moved to whether things would ever return to “normal.” The inertia holding companies back from fully building out their digital infrastructure appears as present as ever when the future appears so unclear.

Despite this inertia, amid a consensus on moving towards a “next normal,” we see accentuated remoteness solved by increased means for infrastructure to manifest digital proximity. On the one hand, many financial institutions are regretting under-investment in digital over the past decade. But on the other hand, with rates slashed, capital is still cheap.

The combination of high incidence of regret, low-cost of capital, and institutional necessity may together catalyze the push financial institutions need to overcome the inertia they face and open the door for more FIs to underwrite capital expenditures on investment in their digital infrastructure.

Segmentation in Infrastructure: Tech Diversification as an Accelerator to Pre-existing Unbundling

Around the same time 10 or so years ago, the financial services industry started to see the ‘great un-bundling.’ Thanks in part to infrastructure companies like Plaid and Stripe, this democratized the ability to create financial services products and risked prizing some while commoditizing others.

The delivery of financial services such as lending, value storage & transfer, investment management, etc. was no longer limited to banks and brokerage firms. Traditional value chains saw a shift in their segmentation.

In a post-COVID world, we expect to see some further re-bundling as incumbents move to adopt advanced tech (e.g., robotic process automation (RPA), blockchain, AI applications and machine learning) that did not previously exist as a core component of their stack, bring these in-house and on that basis develop new capabilities.

Such developments could kick off the latest in what has been a series of shifts in the segmentation of value chains across financial services. Look no further than the recent acquisition in the wealth management space with Schwab acquiring Motif or the Forge <> SharesPost merger. Outside of FS, a prime example of COVID-19-induced value chain consolidation can be seen in Uber’s pursuit of Lime and Grubhub.

Thriving through Collaboration: Where Financial Incumbents and Startups Intersect

We have always believed in the power of the incumbent in financial services. We have never questioned their capacity for survival. Incumbents hold massive advantages over a startup; to name a few: data (i.e., customer preferences), access to infrastructure, and subject-matter expertise. That is not to say that a fintech startup does not stand a chance in the industry, either. In this way, we believe in the power of collaboration. We see a compelling opportunity for incumbents to partner with startups to drive a financial infrastructure that supports a digital-first delivery across all sub-sectors.

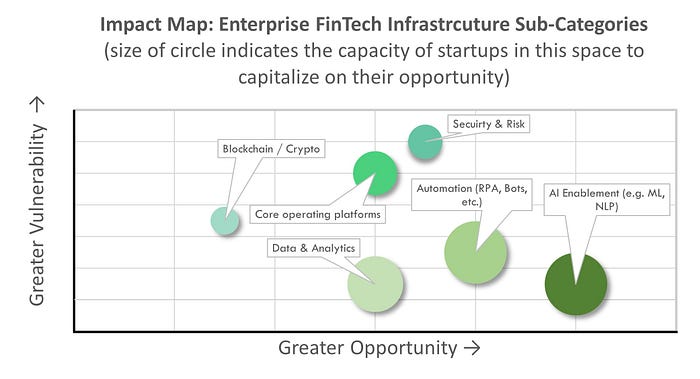

The graph below compares, at a high level, how the sub-categories within Financial Services Infrastructure are experiencing opportunity and vulnerability amid the COVID-19 pandemic and charts the potential capacity players in these segments possess in their efforts to capitalize on that opportunity.

The breakdown of FS infrastructure into sub-components is across technical capabilities like AI and automation, as well as functional areas like security & risk and core operating platforms. The graph plots how we observe a selection of these sub-categories experiencing both opportunity (x-axis) and as well as vulnerability (y-axis) amid the COVID-19 pandemic. The size of each sub-category’s circle indicates the greater (or lesser) potential capacity that players (including startups) in this space possess in capitalizing on or the opportunities presented. In short: which sub-categories could be primed for big shifts?

Machine learning, natural language processing (NLP), and similar technological capabilities that serve as the foundation for deploying AI across processes are poised to attract continued interest from incumbents and investors alike. Second to AI enablement, capabilities like RPA and chatbot implementations are positioned to help drive the continued fervor around automation. The core value prop of both AI and automation are the promises of cost reduction, increased speed of delivery, and hyper-personalization, all of which incumbents across the FS industry have needed for some time, already, and now more than ever are yearning for.

Against this context, it is no surprise that there a great many startups bringing AI capabilities and automation solutions to the market.

So how does an investor focusing on this space cut through all the noise? AI solutions that combine deep domain expertise with technical know-how and execution savvy consistently rise to the top of our lists.

It’s one thing to be able to build an ML algorithm; it’s another thing to have deep industry subject-matter expertise around that ML algorithm which can bring it to life in the real world of the post-COVID Financial Services enterprise.

One of the wittier internet memes over the past several months leveled at the C-suite sums up the state of enterprise financial services infrastructure goes something like this:

“Who led the digital transformation at your company? Select one: CEO, CIO, COVID-19.”

While there are some bright spots to point to around the key role that industry infrastructure played to support the move to a fully remote environment, COVID-19 has also exposed many aspects of FS infrastructure that need further investment and digital acceleration.

Other articles in this series:

Series Header: Impact of COVID-19 on the Areas in which we Invest

[1] https://www.cnbc.com/2020/05/27/coronavirus-crisis-mobile-banking-surge-is-a-shift-likely-to-stick.html

[2] https://techcrunch.com/2019/04/24/microsoft-beats-expectations-with-30-6b-in-revenue-as-azures-growth-continues/

[3] https://www.businessinsider.com/amazon-earnings-aws-amazon-web-services-10-billion-quarterly-revenue-2020-4